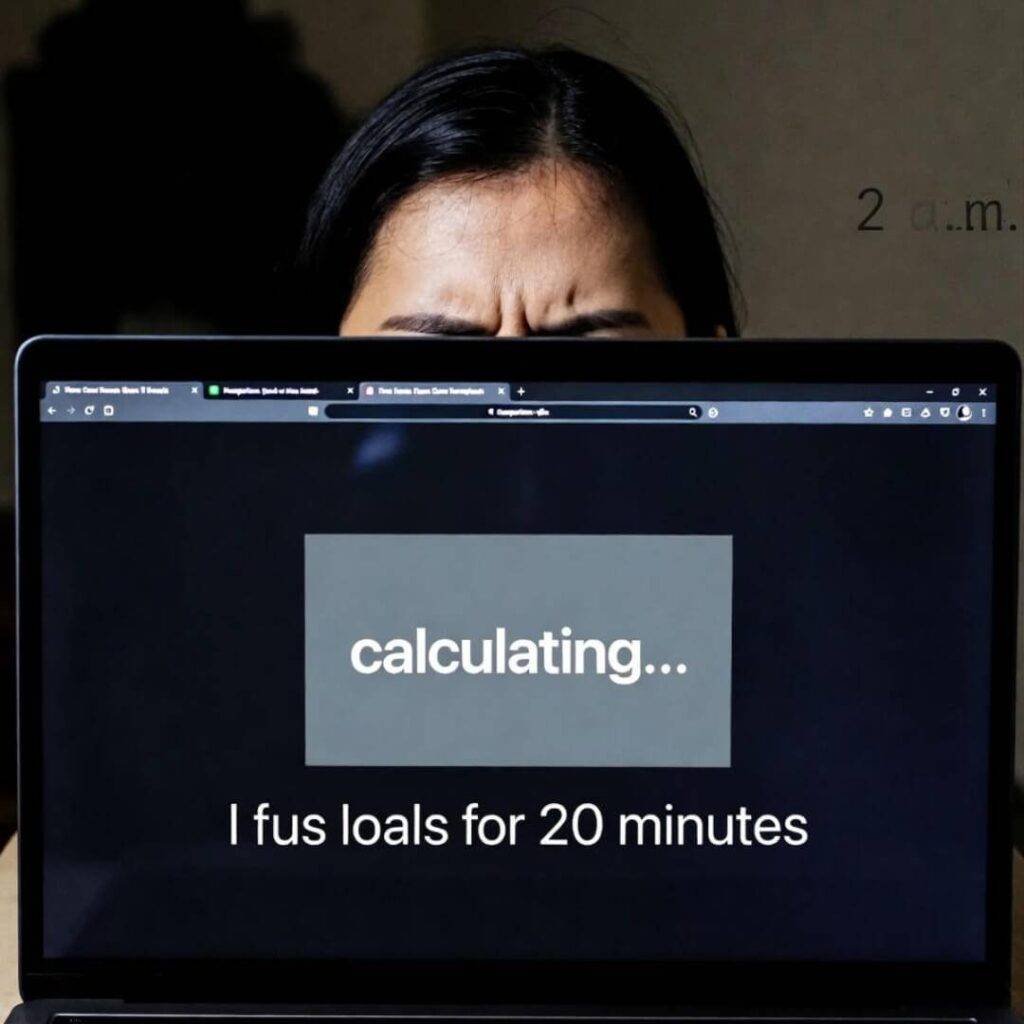

Are car insurance quotes accurate? Man, I wish someone had slapped me across the face with that question before I renewed last month. I’m sitting here in my apartment in Austin—November 09, 2025, it’s like 72 degrees outside which is bullshit for “fall,” and my AC is still humming like it’s July. Anyway, I’m staring at this Geico quote on my phone that says $92 a month, and I’m thinking, sweet, I’m winning at adulting. Fast-forward two weeks: actual bill hits 148 bucks. Like, what the actual hell?

Why My Car Insurance Quote Accuracy Went Straight to Voicemail

So here’s the tea—I’m not some finance bro. I’m just a dude who moved to Texas two years ago, still figuring out why everything’s bigger here except my bank account. I got quotes from like five places: Geico, Progressive, State Farm, some rando app called “InsuraPal,” and Allstate because their ads make me laugh. All of ‘em swore up and down their car insurance quotes were accurate. Spoiler: they lied. Or, like, kinda lied. More on that.

I remember this one night—smelled like Whataburger grease and regret—I’m in my car outside the laundromat, inputting my info into three different sites. Same ZIP code (78745), same 2016 Civic, same clean-ish record (okay, one speeding ticket from 2023, sue me). Quotes ranged from $79 to $201. Two. Hundred. And one. I almost yeeted my phone into traffic.

The “Soft Pull” That Felt Like a Hard Kick in the Nuts

Here’s the thing nobody tells you: most online car insurance quotes? They’re using soft credit pulls and estimates of your driving history. Like, they’re guessing. I found this out when I actually called Progressive—shoutout to Karen in retention who sounded like she’d rather be anywhere else—and she goes, “Oh, the online quote didn’t factor in your garage parking or that you’re not married.” EXCUSE ME? I’ve been garage-parking my car since I moved here! And yeah, I’m single, but that shouldn’t jack my rate 30%.

- Pro tip from my dumbass: Always ask if the quote is binding or just a “soft estimate.”

- Also: Put in your exact mileage. I rounded down from 12,300 to 12,000 and it bit me later.

My Car Insurance Quote Accuracy Nightmare in Bullet Points (Because I Can’t Even)

- Got a $88 quote from Liberty Mutual. Final bill? $137. Reason: “Multi-policy discount not applied without renters insurance.” Bruh, I have renters insurance. With you.

- USAA quoted me $104 but then added a “new resident surcharge” because I moved states less than 36 months ago. Cool, punish me for chasing tacos.

- That InsuraPal app? Straight-up ghosted me after I uploaded my VIN. Still waiting on that “instant quote,” buddy.

How I Finally Got a (Mostly) Accurate Car Insurance Quote

Okay, so I’m not completely hopeless. After the third quote mismatch, I did this weird thing called… talking to a human. I know, wild. Called State Farm, spoke to this guy named Miguel who sounded like he actually drives a car. Told him everything: my dumb speeding ticket, the fact I parallel park like a raccoon on Red Bull, how I only drive to H-E-B and back. He ran a hard quote—yes, it dings your credit a tiny bit—and boom: $119. Locked in. No surprises.

My Dumb But Working Checklist for Reliable Car Insurance Quotes

- Call, don’t click. Online tools are like dating apps—90% lies.

- Screenshot everything. I have a folder called “Insurance Lies 2025.” It’s… robust.

- Ask about “final rate triggers.” Some companies wait till you sign to add fees for “low mileage verification” or whatever.

- Bundle, but don’t get suckered. My renters + auto saved me $18/month. Worth it? Eh.

The One Time a Car Insurance Quote Was Too Accurate (And It Freaked Me Out)

True story: I used this sketchy comparison site—won’t name names, but it rhymes with “SchmolicySchmenius”—and the quote was spot-on. Like, to the penny. $126.48. Final bill? $126.48. I was so shook I called to confirm they didn’t hack my bank. Turns out they partner with one specific carrier and only show binding quotes. Rare, but it happens.

Wait, Are Car Insurance Quotes Accurate Ever?

Here’s my unfiltered take: No. But also yes. They’re accurate enough to shop with, but treat ‘em like weather forecasts—bring an umbrella. The final number will change. Always. Unless you’re Miguel from State Farm and you’ve got a human who isn’t a robot.

Look, I’m still salty. My coffee’s cold, my dog’s judging me, and I just found a new quote for $107—but I’m not clicking “buy” till I call. Learn from my chaos, y’all.

Your move: Grab your latest quote, call the number, and ask, “Is this the real price?” Then tell me in the comments if they laughed, cried, or hung up. Let’s expose these quote goblins together.

(P.S. I linked some actual resources below so I don’t sound like a total conspiracy nut. You’re welcome.)

{kind=link}