Okay, lemme spill this tea while the Bengals game loads in the background and my dog keeps farting on the couch. Online car insurance quotes straight-up rescued my broke ass last month and I’m still kinda mad I waited until I was 32 to figure this out. Like, I was paying Allstate $214 a month for full coverage on my dented Civic that smells like gym socks and regret. Two Skyline chilito runs and one panic attack later, I’m down to $97 with Progressive and I feel like I just discovered fire.

How I Screwed Myself for Years with “Loyalty” (Spoiler: Insurance Companies Don’t Love You Back)

Bro, I stuck with Allstate since I was 19 because the agent was my buddy’s mom and she gave me a stupid keychain. That’s it. That’s the whole reason. Meanwhile I’m eating Aldi brand cereal and skipping oil changes to afford the premium. Last week I’m sitting in the Walmart parking lot off Fields Ertel, rain smashing the windshield, chili cheese fries sliding off the dash, and I finally snap. I Google “online car insurance quotes” like a degenerate at 3pm on a Tuesday.

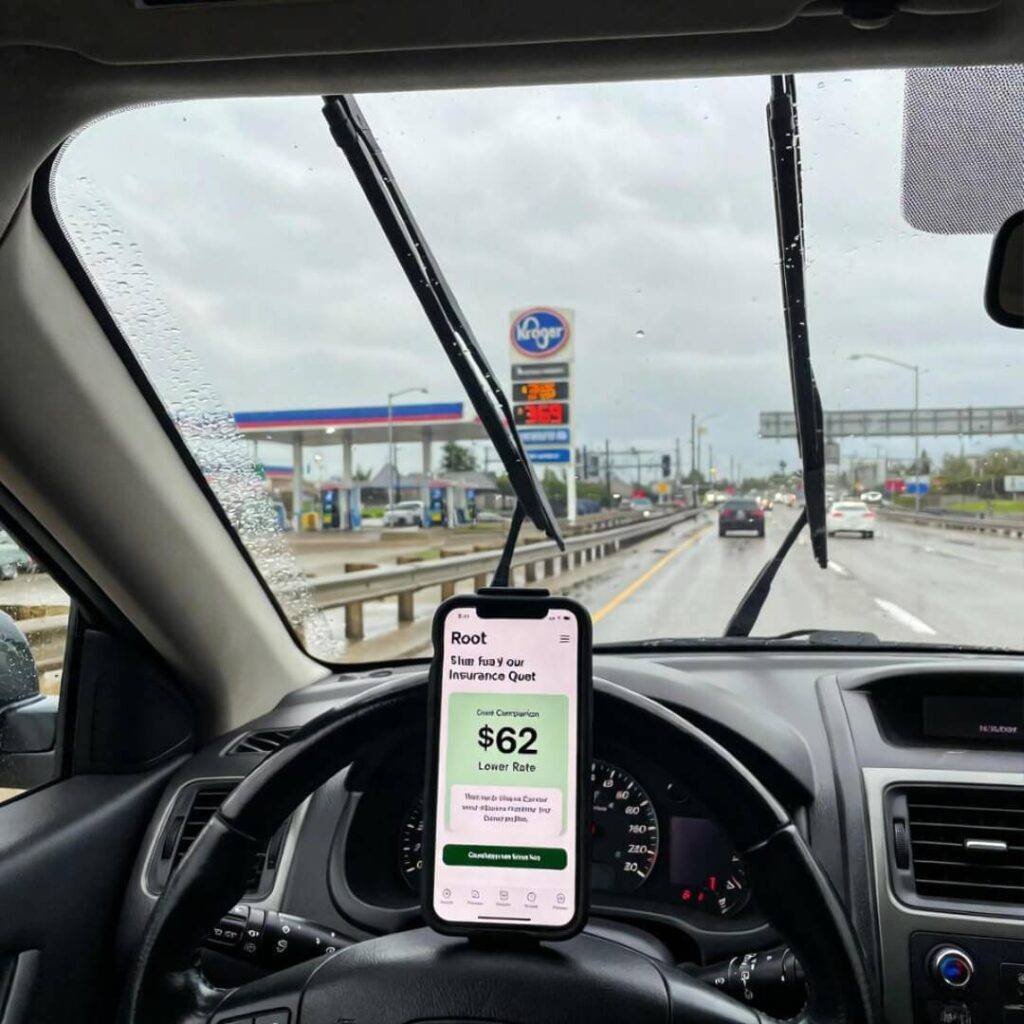

Ten minutes in I’m shaking. Geico wanted $142, Progressive $97, Root $89 if I let them track my driving (which, lol, they’re gonna see I drive like I’m fleeing the law, but whatever). State Farm still quoting me $198 like I didn’t just watch my roommate get rear-ended by a deer last year.

The Exact Dumb Steps I Took to Compare Car Insurance Online (You Can Copy-Paste My Chaos)

Here’s the unhinged play-by-play, zero filter:

- Opened every quote site in incognito so they couldn’t price-creep me (yes I’m paranoid)

- Lied a tiny bit about mileage because I deliver Uber Eats when I’m drunk on weekends, fight me

- Put my credit score as “good” instead of “haunted” – turns out that matters more than driving record??

- Added my girlfriend as a driver even though she doesn’t have a license yet because it dropped the quote $23 somehow

- Took Progressive’s stupid snapshot thing and drove like a grandma for two weeks – saved another $31

Literally twenty minutes. I screenshot everything because I thought it was a scam. Called Progressive at 2am from the Meijer parking lot because I don’t sleep normal hours. Lady confirmed the $97 quote and I switched on the spot. Cancelled Allstate the next morning and they tried to guilt me with “loyalty discount” – ma’am I’ve been loyal to Skyline Chili longer and they don’t charge me $214 for a three-way.

The Mistakes I Made So You Don’t Have To (Free Auto Insurance Quotes Edition)

- Waited until my policy renewed like a chump – you can switch mid-term and get prorated refund

- Forgot to ask about disappearing deductibles (Progressive dropped mine $100 each year I don’t crash)

- Almost fell for those “enter to win $500 gift card” quote traps that sell your data to 47 companies

- Didn’t bundle renters at first – added it later and saved another $19 somehow

Also pro tip: do this drunk on a Thursday night. The quotes are the same but you care less about entering your VIN twelve times.

Why Cheapest Car Insurance Isn’t Always Sketchy (My Progressive Hot Take)

Root tried to charge me $89 but then wanted my blood type and firstborn child for tracking. Hard pass. Progressive gave me $97, forgave my 2019 speeding ticket in Kentucky (don’t ask), and their app doesn’t make me wanna yeet my phone. Also their commercials with Flo still slap and I’m not ashamed.

The Moment I Realized I’d Been Getting Robbed for Literally a Decade

When Allstate sent the refund check for $312 for the unused portion. Three hundred dollars. That’s like… sixty-three Skyline coneys. I sat in my driveway crying into a Taco Bell bag because I’m a 32-year-old man who just learned capitalism is a scam.

Switching Car Insurance Mid-Policy: The Part Where I Panicked Needlessly

Thought I’d have a coverage gap or something. Nope. Progressive started the same day, Allstate cancelled gracefully (after trying to sell me life insurance, read the room Susan). Printed new cards on my janky HP printer that sounds like it’s dying. Taped one to my dashboard next to the chili stain like a trophy.

Instant Insurance Quotes Are Crack for Broke Millennials

I now check online car insurance quotes every Sunday night like it’s fantasy football. Got Root down to $84 last week but they wanted my Spotify data or something? Bro I’m not giving you my sad boy hours playlist for $13.

Look, I’m still the same idiot who parallel parks like I’m solving a Rubik’s cube blindfolded, but my bank account is $117 richer every month. That’s concert tickets. That’s therapy. That’s not crying when Kroger gas hits $3.79.

If you’re still paying more than $100 for basic coverage on a 2012 Civic that’s 40% duct tape, do yourself a favor – grab your VIN, your social (kidding, don’t do that), and spend fifteen chaotic minutes comparing car insurance online. Worst case you waste a Red Bull. Best case you’re eating steak instead of Aldi ravioli for once.

Here, I’ll make it stupid easy – start with these (I get nothing for this, I just hate seeing friends get robbed):

- Progressive quote tool – took me 7 minutes

- The Zebra – compares like 20 companies at once

- Geico – 15 minutes could save you 15% or more (their jingle lives rent-free in my head)

Do it right now while you’re supposed to be working. I believe in you, fellow financial disaster.

Now if you’ll excuse me, the Bengals are down by 14 and my dog just farted again. Adulting is undefeated.

{kind=link}